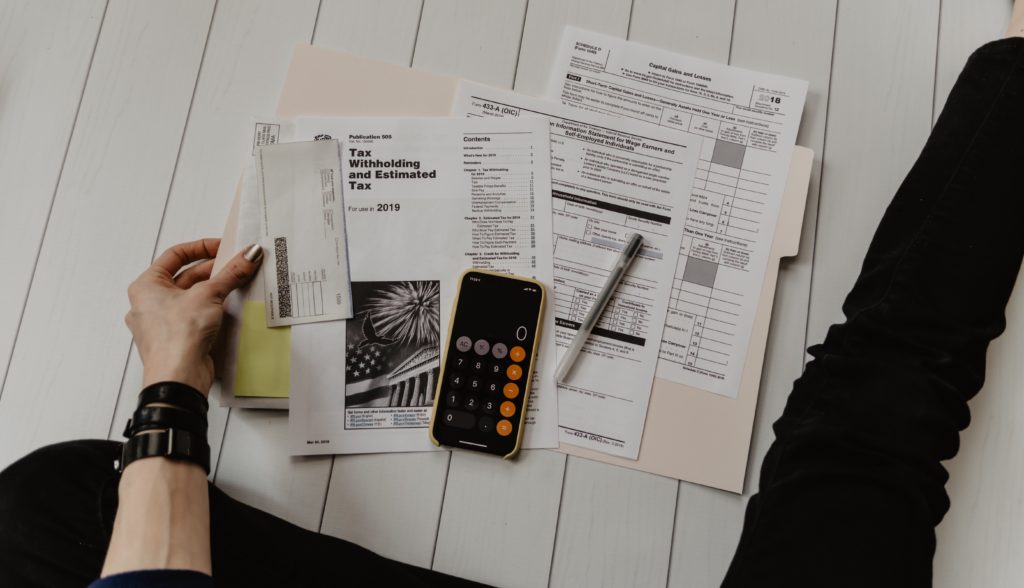

It’s understandable that people want to save money, whether it’s on individual federal taxes or when keeping records for a business throughout the year. Many individuals are seriously debating whether to purchase professional accountant-level software or to hire an accountant. There’s really no comparison – hire an accountant.

Tax Accountant

Hiring an accountant minimizes the potential for an error and significantly reduces the danger of getting audited. Those with highly complicated tax situations involving stocks, bonds, investment income, dividends, and even cybercurrency are best served by an accountant. Professional accountants have worked with industry-grade software for years and even decades. They know exactly how and where to enter figures, and are familiar with all the terms used.

Tax accounts are highly trained professionals. They’re knowledgeable about all aspects of tax law, have the benefit of experience, and continuing education. They can provide advice about investments, credits, deductions, and tax planning to lower an individual’s tax burden, while helping clients to more effectively manage their finances. Accountants are available throughout the year to offer advice and answer any questions clients might have as they arise.

Tax Software

Many individuals believe that if they have accounting software like professional accountants use, their problems are over. Accounting software like the experts work with varies widely in cost. Some have a one-time cost per user of up to $999 per year. That’s just for the software. It doesn’t include licensing fees.

There’s also a steep learning curve for a non-accountant. Professional accounting software is highly sophisticated, with terms and abbreviations with which the average individual won’t immediately be cognizant.

Individuals trying to use accountant software can easily find themselves in the 4 percent of taxpayers that are audited. The risk of an audit is elevated if an individual has income exceeding $200,000 per year, is a sole proprietor of a business, or has foreign assets. Non-accountants trying to use professional accounting software are increasing their risk of an audit.

At Peavy and Associates PC our mission is to assist you with all your tax preparations, payroll and accounting needs. We provide our clients with professional, personalized accounting services and guidance in a wide range of financial and business needs. Give us a call today (843) 347-0849 and discover why our clients return to Peavy and Associates, PC year after year!